- Reputation, or your credit. How well have you do title loans do credit checks in Texas paid back other people? And that's determined by the type of trade lines that you have on your credit, what your credit score looks like.

Why don't we just say in annually of today, rates of interest was plenty best and you've got tax productivity to prove your revenue, you can always refinance a loan with the a conventional financing, FHA loan otherwise a bank report financing

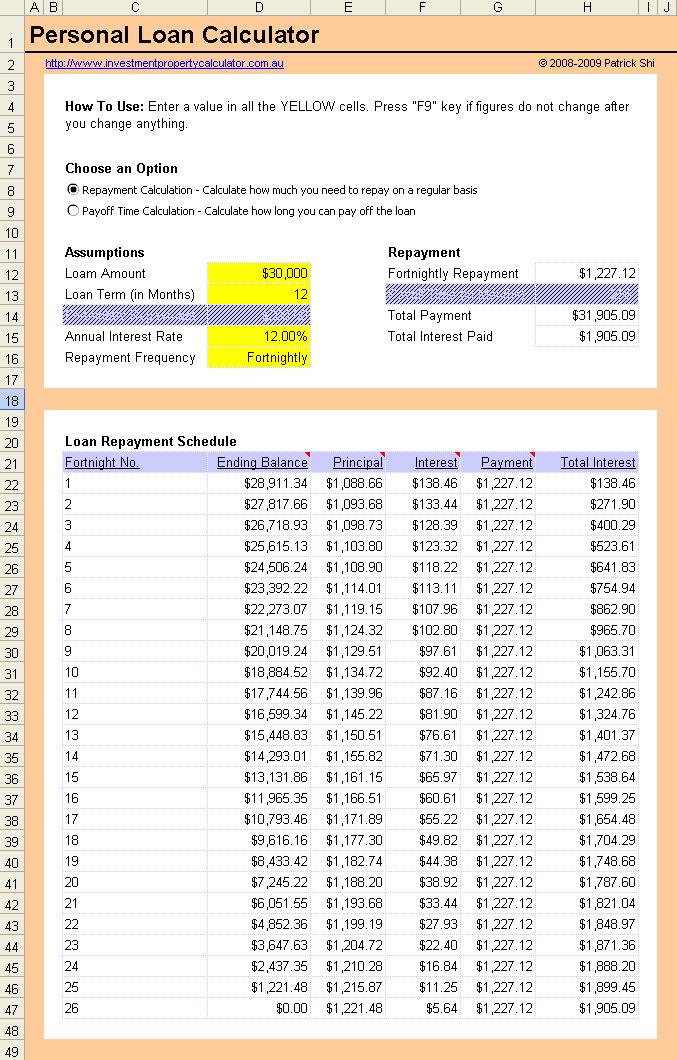

![]()

- Capacity or Income, We look at normally on a full-doc loan or on a bank statement loan. We can look at income a few different ways, though. We can look at it with tax returns, we can look at it with bank statements. For a cash flow loan, We can look at the income of the property itself, with the amount of income that it's coming in as a rental for cash flow.

3. Financing, which is your skin in the game, right, and that's very important. So, back in 2008, you could buy a house with no money down.

Now, everybody means a deposit, therefore having a normal mortgage, can be done as low as step three% down, 5% off.

Reserves was a thing that suggests how much money/savings you really have remaining, after you produced their advance payment and you may paid down their closing costs.

Let us merely state inside the a year of today, rates of interest is actually really better and you have taxation efficiency to prove your revenue, you can refinance that loan to your a traditional financing, FHA financing or a lender report loan

- Guarantee, which is the property itself. What is the condition of the property, how many bedrooms and bathrooms, where is it located, is it on the beach or in the town or, is it on 10 acres, or is it a single-family residence or a condo or a duplex or 4 plex?

So, all of these 4 C's are the basics for a no-doc loan. All would apply, but you would just take out capacity or the income piece.

Jackie Barikhan: Imaginable where in fact the investors who buy these types of funds... hedge funds, insurance agencies, Wall Street guys, they look on a risk-award basis.

So without a doubt, in the event the we are not demonstrating income, it's a little riskier proposal. Therefore, for this number of most risk, they are going to select more go back to the the rate.... but it is not like difficult currency.

Already () we're in about a seven% interest diversity having the full doctor financing, in which you amuse W2's/ tax statements.

If you performed a bank report loan, those interest rates would be rather equivalent, sevens and you can eights, probably. Thus, regarding a point approximately above the markets.

The fresh new zero-doc device is probably another type of area more than one to. Thus, probably eights and you can nines now. There are also options to pick rate into the 6's.

Jackie Barikhan: Proper, as well as you've got the expenses associated with difficult currency usually three to four issues etcetera...

Very, our the-cash customers, certain kinds of marketplaces for which you receives a commission numerous bucks or you just cannot file it otherwise almost any

Restaurant customers, the new cannabis industry, latest divorces. We'd men which was promoting those people gorgeous highest-stop athletic shoes, and he is promoting them on the web. The guy did not really have the bank statements to display one, however, he was making many currency, in which he had a great down payment, he previously sweet supplies.

When we can be meet the requirements you having a lesser interest rate, that have a special program, obviously, we shall do this for your requirements.

I recently had a customer which was only doing a corporate. Very their lender statements for his team were not most exhibiting sufficient income yet, however, he was increasing, and also you could see the organization, doing best and higher. The guy did not quite feel the one year from lender statements in order to qualify, to-do a financial report loan.